Andriy Belen

Insurance Expert

Enter your ZIP Code

to get insurance quotes in your area

Today's modern life is so multicomponent and eventful that, at times, we do not notice things and events that are really important. Especially if they affect our lives, not obviously or, in the long term. The consequences of this blurring of our attention can be unfortunate. But, proper housekeeping and personal financial affairs can neutralize all the unpleasant results. In the case when it concerns the state, the consequences can be too severe and unpleasant.

But this is not the worst. The disaster is that the state machine is very clumsy and unwieldy. And its steps are incredibly long, and the gears of the system are spinning very slowly.

This is undoubtedly the price to pay for the most elaborate checks and balances system that our greatest country created. The state structure can be criticized endlessly, but the truth is that today there is no more advanced and perfect democracy in the world. And this is another reason we find an adequate response to global challenges so slowly and out of time.

It is unlikely that it will come as a surprise to you that literally, every state has laws that seem strange today.

For example, Little Rock, Arkansas has a law that "no person shall sound the horn on a vehicle at any place where cold drinks or sandwiches are served after 9:00 p.m." Yes, this means that if you start honking near Subway, then the police have the right to fine you.

And in the state of Delaware, there is a rule that prohibits whispering in church. This is interpreted almost as a violation of public order and is subject to severe punishment. And how about the Georgia law that prohibits the use of a knife and fork when eating fried chicken? Thinks this is absurd? Nope. Not so long ago, in 2009, one poor fellow was even arrested for violating this requirement.

There are many urban legends on the web describing ridiculous laws of different US states. Naturally, most of this news is fake, but it is obvious that there is no smoke without a fire. And the above examples prove it.

No matter how ridiculous it may sound, such seemingly meaningless norms often have logical prehistory, and there was even a need for them. Some of them were adopted based on the necessity and realities of that time. Others were taken out of a desire to choose the simplest path. The bottom line is that to remove these norms from the regulatory framework. You need to go through a difficult bureaucratic path that is not universal for every state or county. The bottom line is that some of the laws passed in the nineteenth century were relevant and seemed acceptable. Today, their relevance is lost, but the system is too clumsy to get rid of this ballast.

What can we say, even if our electoral system is regularly subjected to severe criticism? If you do not delve into the problem, it seems that this criticism is fair and justified. Indeed, in the 21st century, electing a president using a complex and incomprehensible scheme with an electoral college is nonsense. In any case, this is the opinion of most foreign observers who do not seek to get into the realities of the United States.

And the reality is that in those days when such an electoral system was born, it was justified and, perhaps, even optimal for the country of that time. And the current archaism is not the stupidity and lack of foresight of the creator of the system, but the heavy state system's inability to react in time to the changed circumstances.

The same disease hurts all of us when it comes to economics. On the one hand, the US financial system is incredibly sophisticated, competitive, and multifunctional, especially compared to other advanced states. On the other hand, is it worth recalling the catastrophic crises and failures that occur with alarming frequency? And we would like to understand these problems since they usually arise precisely from the slow reaction of a cumbersome state system. And our conversation today will touch on one of the leading sectors of the economy, both in monetary terms and in social importance - the insurance industry, its problems and unhealthy correlation with financial growth.

The meaning of the insurance sector in the economy is a very vague concept. Its paradox lies in the fact that we cannot objectively assess its role on a global scale. The truth is that this industry has not been perceived as a separate and independent element for a long time. Moreover, until 1993, analysts considered insurance no more than a part of the industrial sector in national accounts. Many scholars viewed the industry as part of the banking sector. And, in general, the industry was perceived as parasitic and not independent.

For many, this point of view persists to this day. Although, it must be admitted that today such opinions are not very popular, and the consequences of the pandemic and crises of the past decades have radically changed the assessment.

You don't need to be a professor of macroeconomics to appreciate how important insurance is. All you need is to imagine that insurance companies, like the insurance institution, have disappeared from the market. If not a national collapse, all this will lead to the collapse of hundreds and thousands of mechanisms that have facilitated and cemented the market.

In addition to the obvious and measurable in money functions, insurance also has an invaluable function that cannot be adequately measured in numbers. We're talking about predicting and minimizing potential risks. This immeasurable mechanism has a key and critical role in economic growth.

Economic growth, classical science is defined as a symbiosis of growth, quantity, and efficiency of labor and the economy's capital intensity. It is quite clear that this is a complex process, which is influenced by many factors, most of which cannot be predicted and, at first glance, look like chaotic processes. Therefore, even a fraction of a stable probability can increase the probability of a forecast and reduce investment and other risks in such calculations. And this is where the insurance industry enters the field, bringing stability to the Brownian movements of some financial mechanisms.

With a firm ground in the form of mitigating potential shocks, market actors are empowered to make decisions with mitigated risk. And thus, in the form of the insurance industry, we get a key but not obvious and hidden factor in economic growth theory.

Despite the theory's status, we can find enough confirmation of it both in history and in modern times. For example, in Great Britain, since the beginning of the industrial revolution, the relationship between GDP growth and the introduction of insurance into economic processes has been clearly traced. These facts are also confirmed by research as biased organizations.

All this looks very logical, given that all business activities are associated with decision-making that has uncertain risks and is fraught with material losses. And in our case, personal and collective risk management strategies come to the fore. Thanks to well thought out strategies, even minimizing losses becomes an acceptable result.

All the consequences of such activities cannot be described in one article. And not only because of the lack of space but also because the entire spectrum of influence of these non-obvious mechanisms has not yet been studied and systematized in global economic science. But, in general, we can think about this web for a very long time, and each time we find new points of contact of insurance with all horizons of the financial system.

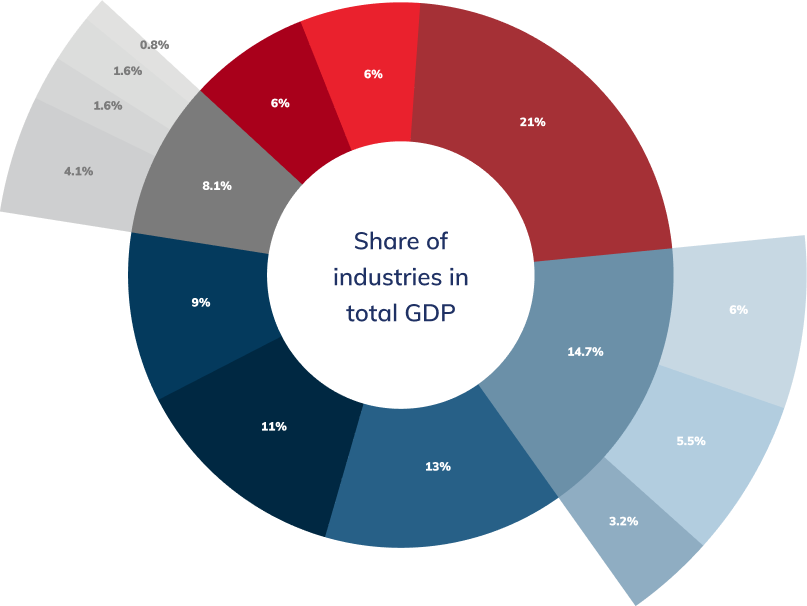

Moreover, the insurance industry also ensures the state, acting as a stabilizer. Moreover, this role becomes critical in the event of unpredictable disasters. It is difficult to overestimate. For example, in 2013, the loss from natural and human-made disasters amounted to $ 140 billion. Insurance companies compensated a third of this astronomical amount. More importantly, there was no global industry collapse, and the sector continued to exist, developing and strengthening its share in GDP. And speaking of GDP, it is worth illustrating the statistics graphically, according to which an incredible 21 percent is occupied by insurance, finance, and real estate.

The industry that makes up Wall Street (finance, insurance, and real estate) is the biggest contributor to GDP

Also, insurance accounts for the penetration rate of the main markets in the US. Moreover, according to Sigma, its level varies from 7.23% to 8.40% depending on the year, but this is not important. On a US scale, this figure is almost a point ahead of the general trend, and from developed countries, it is higher only in Japan.

| 2000 | 2007 | 2017 | |||||||

| Life | Non Life | Total | Life | Non Life | Total | Life | Non Life | Total | |

| United States | 4.20% | 4.20% | 8.40% | 4.20% | 4.70% | 8.90% | 3.12% | 4.11% | 7.23% |

| China | 0.80% | 0.70% | 1.50% | 1.80% | 1.10% | 2.90% | 2.68% | 1.86% | 4.57% |

| Japan | 8.60% | 2.10% | 10.7% | 7.50% | 2.10% | 9.60% | 6.26% | 2.34% | 8.60% |

| Europe | 5.10% | 2.70% | 7.80% | 5% | 3% | 8% | 3.77% | 2.68% | 6.45% |

| World | 4.60% | 2.70% | 7.30% | 4.40% | 3.10% | 7.50% | 3.33% | 4.11% | 6.13% |

A very objective indicator is the gross domestic product (GDP) - the total monetary or market value of all finished goods and services produced within the country for a certain period of time. This value serves as a kind of thermometer for the country's economy.

The relationship between insurance density and GDP growth is obvious and has its own rules. In emerging economies, insurance growth usually exceeds GDP growth. With its own communist-capitalist vector of development with a local flavor, only China gets out of these laws. Simultaneously, according to Sigma, the figures for the United States are very indicative and show a decline only in 2013, when, as we have already mentioned, the number of payments was huge.

| 2000 | 2007 | 2009 | 2011 | |||||

| GDP | Ins. | GDP | Ins. | GDP | Ins. | GDP | Ins. | |

| United States | 1.00% | 7.20% | 1.80% | 4.54% | -2.80% | -5.98% | 1.60% | 5.60% |

| China | 8.50% | 32.20% | 14.20% | 30.74% | 9.30% | 15.78% | 9.60% | 3.30% |

| Japan | 2.50% | 22% | 1.20% | -2.63% | -2.20% | 4.70% | -0.10% | 14.70% |

| Europe | 4.10% | -2.30% | 3.70% | 15% | -4.30% | -5.46% | 2.30% | 2.23% |

| World | 4.20% | -1.48% | 4% | 10.50% | -1.60% | -3.64% | 3.20% | 5.90% |

| 2013 | 2015 | 2017 | ||||

| GDP | Ins. | GDP | Ins. | GDP | Ins. | |

| United States | 1.70% | -1.31% | 2.90% | 3.12% | 2.30% | 2.86% |

| China | 7.80% | 13.28% | 6.90% | 17.70% | 6.90% | 16.16% |

| Japan | 2% | -15.19% | 1.40% | -5.60% | 1.70% | -6.50% |

| Europe | 0.80% | 5.91% | 1.80% | -13.30% | 2.60% | 2.09% |

| World | 2.60% | 0.91% | 2.90% | -4.20% | 3.30% | 4.01% |

The penetration of insurance into all layers of social life is simply incredible. Thanks to this tool, savings, and retirement income are protected. Mortgage insurance softens the impact of unemployment on ordinary citizens. Therefore, it stabilizes the household's cash income, preventing it from falling off the cliff, which, in turn, is reflected in the weak amplitude of economic fluctuations.

To summarize all of the above, we can confidently say that the insurance segment is the most important part of our economy, unique in its versatility and flexibility. From the state's point of view, this is one of the most amazing elements of maintaining economic performance at the required level. And in a global sense, it is a kind of analog of a constant variable. But, what about influence at the lowest level of interaction? At the level of an ordinary taxpayer.

Insurance in the United States is part of the risk market, which is the largest in the world in terms of premiums. Of the $ 4.640 trillion in gross premiums reimbursed globally for the 2013 period, 27% is in the United States. This is an incredible amount of $ 1.274 trillion in monetary terms, even with a reservation on the facts that we mentioned above.

The history of the insurance industry in the United States began in the middle of the 18th century when the first company opened in South Carolina, similar to risk assessment and monetary compensation when certain events occurred. One of the industry pioneers was Benjamin Franklin, whose versatility and genius can hardly be overestimated. It was he who stood at the origins of the oldest company in the country.

At the end of the 18th century, the first joint-stock insurance company appeared in the United States. In the 30s of the next century, the formation of the legislative framework for regulating the industry began. With the first appointment of an insurance commissioner two decades after the first law was passed, the next major milestone came in the 1950s. When the laws began to permit multi-line charters, it became an impetus for the industry's development and a powerful boost for its growth.

Today, the insurance industry in the USA is divided into several groups, the most important of which is life (including long-term care, accidental death, and dismemberment, hospital indemnity) and health (including dental, vision, medications, others) insurance, which is the largest and most controversial part of the market. Besides, the industry includes annuities (securities), life and annuities, property and casualty, property (flood, earthquake, home, auto, fire, boiler, title, pet), casualty (errors and omissions, workers' compensation, disability, liability). At the same time, usually, reinsurance is singled out as a separate type of service.

Summing up the interim results, we note the following: the insurance industry is one of the most important economic elements. Its role in the financial system is so great that it is tough to find similar industries' influence in other countries. The flexibility and multifunctionality of influence on the economy's general picture are comprehensive and difficult to assess. And this is probably good news. Now let's move on to the bad ones.

As a multifaceted and non-standard tool, the insurance industry could not afford routine and boring problems. To understand them, they write monographs and books. But, we will try to outline the scope of these problems because we will need to solve them for a long time, simultaneously fighting the clumsiness of the monstrous state machine.

So, when the industry began to take on the shape of a full-fledged and confusing sphere in the late 19th century, new insurance products appeared. Naturally, it was difficult for society to grasp all the subtleties of the new intriguing sphere of the modern market, whose goals were very logical and seductive. The result was the deliberate complication of anything that could be complicated. There were all possibilities for this since there was no government regulation. And those regulatory legal documents that existed were rather nominal and left a huge space for manipulation. And where there is room for manipulation, there are scammers.

Speculation and irregularities were enormous and varied. From banal companies that did not have the capital to cover liabilities to unreasonably high premiums. Needless to say, about wild competition, where the participants did not understand the methods, to create their own monopoly?

In a neat addition to the chaos that was going on, the essence of insurance was ideally suited to Ponzi schemes (https://www.investopedia.com/terms/p/ponzischeme.asp). Because of this, financial pyramids with insurance slogans began to appear at an astronomical speed.

An adequate response was essential. But, it followed at the state level, which tried to curb the ongoing chaos in various ways. But, to solve the federal problem, the participation of federal institutions was required. It would seem an obvious truth. But, it took 35 years to master it, until, finally, the Social Security Act, which provides for the payment of unemployment benefits and retirement benefits, came into force.

This Act, at one time, was like an explosion. According to the government, he had to solve the problem, and in a very unexpected way. Considering insurance companies a significant share of their market under state regulation, the document should have scared other market participants. And, the industry had to start regulating itself. What could make her do this? Fear. The fear that the state will interfere in the affairs of the industry is even stronger. It would seem that the idea is dubious, but it brought its results.

Natural selection made its own adjustments with the outbreak of World War II. After the Great Depression and the beginning of the global conflict-affected all spheres of public life, the plight of the economy. Wages were frozen, and insurance companies tried to attract workers by any means possible. At this time, group life and health insurance policies appeared. However, only large companies could offer such large projects with substantial financial guarantees. And this, it would seem, is not bad, but small enterprises were practically destroyed in this struggle.

This state of affairs no longer just attracted attention but threatened to get out of state control. Therefore, in 1944, finally, the Supreme Court issues a ruling according to which the insurance industry should be regulated at the federal level. And this was the correct and balanced decision, which laid the foundation for the industry's objective regulation.

Until 1945, rather, before Congress passed the McCarran-Ferguson Act, which brought industry regulation back to the state level.

This state of affairs continues to this day. Is it good? In our opinion, no. Given the social, government, and financial importance of insurance, it is an unaffordable luxury to have various approaches to controlling it. The game rules vary from state to state, antitrust regulation is not effective, and several laws that have followed only increase the number of issues and complicate the interaction with the end consumer.

From our perspective, a huge problem is the conditions for the existence of the insurance industry today—certain segregation and isolation from the general background of the development of the economy and financial institutions. The main prerequisite for this was the McCarran-Ferguson Law. The links that should have leveled off the correlation between the insurance industry and the economy were broken from the start and reinforced in 1945. The result was a very peculiar and special way of development and evolution of this sphere. Is it good? In our opinion, no.

Taking into account today's reality, the policy turns into a direct analog of investments. And in the end, we can get some semblance of a situation that led to a catastrophic real estate crisis. Only the consequences can be much greater.

If the previous paragraph's ending seemed apocalyptic and unrealistic to you, we would like to focus on specific hidden functions that insurance companies perform today. Many of us mistakenly believe that a policy is just a legalized form of taking money, which provides some opportunities to implement if the appropriate conditions come. But, in fact, the degree of insurance penetration into our lives is much wider than you think.

The money supply that companies accumulate from clients is huge. In return, you get financial protection from various domestic troubles, problems with your home, car, or unforeseen injuries.

Businesses and companies also receive protection from unforeseen situations that could lead to employees' bankruptcy and layoffs. This expands investment opportunities for insurers' clients and opens up new horizons for investing in risky projects. And all this is based only on the confidence that the partner will reimburse or share the risks in case of failure.

The agricultural industry, too, is largely built on insurance and short-term lending. And farming is one of the most important segments of our economy.

And now, let's pay attention to another crucial point - insurers, according to the American Insurance Association, have invested more than $ 1.4 trillion in the economy (https://iowains.org/). Often, this is money that was not used for insurance benefits and other operating expenses. By joining the financial system, this money supply in corporate and government bonds, stocks, and mortgage loans directly affect its development. If you were not impressed by the investment figure, then pay attention to what companies' budgets go only to advertising.

This table shows only the main market players. In general, there are far more insurance providers in the country than you might imagine. Of course, the forecast below speaks of a gradual decrease in the number of market players. Firstly, the decrease is insignificant, and secondly, it will take place, most likely, due to mergers and acquisitions.

No matter how pathetic it may sound, the insurance industry is one of the main pillars on which our well-being and confidence in the future are based. We feel a little uncomfortable, realizing that this pillar was erected according to opaque architectural projects and, today, is serviced according to very confusing instructions.

A certain demonic halo has always hovered over the insurance companies, and sometimes it seems that they are quite happy with it. The fake friendliness of advertising campaigns does not always work to create a positive image. Sometimes, this irritates and becomes another reason to spread conspiracy theories in society. Fascinating here is the 2018 poll in Washington about areas that have too much influence.

Additional Information:

United States; Kaiser Family Foundation (Health Tracking Poll); March 8 to 13, 2018

It seems there is nothing wrong with that, and, for now, everything works. But, I would like to have a clear play-book, first of all, to prevent a possible catastrophe in time.

There is a special layer in the multilayer pie of the American insurance system - American health care. Everyone heard it, even people who have not spent a day in the United States. Everyone hears it, and disputes and their nuances are discussed even outside the borders of our country.

The most expensive system in the world. The most unfair health insurance system. Time bomb in a democracy. The clearest proof of the depravity of the capitalist system. Here are just the most striking epithets used by opponents and critics of today's medical realities.

And it's not only about general justice, about which people have been sadly joking for a long time. It would be appropriate here to quote former President Donald Trump, who aptly described the second problem. He said the health care system is "very complex."

Everyone understands this. And, everyone who has come to power in the United States recently promised or tried to solve this problem somehow, balancing the beneficiaries' interests, all layers of society and the state. But, even the list of interested parties suggests that this task is barely feasible. The endless controversy led to Obama's reforms, which were replaced by attempts by Republicans to reform the results of reforms during Trump's tenure. But, the state machine turns slowly, especially when it does not know where to go.

Obamacare is considered by many to be the key to the start of the crisis. Other observers date back to the introduction of Medicare and Medicaid, half a century ago. We tend to agree with the third group of scientists, whose opinion was unified by Christy Ford Chapin, author of Ensuring America's Health: The Public Creation of the Corporate Health Care System.

The opinion of the author and adherents of the third theory coincides with ours. The heart of the problem was hidden in the 30s of the last century when the first serious attempts to regulate insurance activities began.

At the same time, in 1938, serious structural problems arose in the health care system. Too many important events happened during this time, especially in medicine. Treatment and prevention made a giant leap forward: vaccines began to be actively used, the microbial theory began to be recognized by the broad masses, hospitals began to transform, becoming civilized and practical. All this happened in front of ordinary people, in whose memory the consequences of both diseases and treatments, which had been practiced a couple of decades ago, were still alive. Imagine, literally twenty years ago, out of 100% of those suffering from tuberculosis, 80% of young people under 20 died. And today, doctors began to work miracles! Naturally, public opinion quickly supported vital new changes.

Quite understandably, the demand for trained and competent doctors immediately increased. Following this, industry regulators' influence began to grow, primarily the American Medical Association (AMA).

Everything developed very logically. Doctors were divided into conditional categories, depending on their professional level. From this, conditional prices for services were formed. The rules of the game were not established. Therefore, all market participants acted on a whim.

The pricing policy and payment options were set in different ways. And often doctors worked not only for money but also for food and counter services. Humanism was also no stranger to doctors - and many of them assisted in charitable clinics as a social burden.

Some chose a fair model to monetize their knowledge, using a sliding scale payment method. In which the poor patients paid little, and the rich pay more for the same services.

Of course, at first glance, the system worked and even had the beginnings of justice. But, in the end, everyone was unhappy. And first of all, patients who believed that it is better to pay regularly, but in small amounts than once a year, but much more than they could afford. Actually, this is a simplified model of modern insurance, in a nutshell.

The doctors did not mind, and without waiting for the government's reaction, they began to form multidisciplinary group practices, which, in fact, were quasi-insurance formations. Self-help societies and trade union charities have also sensed the coming changes and began to enter the market. After all, no one set the rules of the game.

What could not be done was to use the services of a large insurance company as an intermediary. And such companies existed on the market, and after the tax reform of 1913, their number only increased. But, they were slow to respond to current requests. They felt quite comfortable within their main activity framework - group life insurance and servicing pension plans for the business. It is also characteristic that insurers requested to expand the case of services through health insurance, primarily from businesses. But they considered the new perspectives temporary, and the field of activity risky and difficult to predict.

At the same time, medical industry regulators and, above all, the AMA have closely monitored the situation. Were they sure that all these associations, all third parties that get between the doctor and the patient - a terrible idea? Do you know why? Because the involvement of a third party in this relationship will inevitably lead to a decrease in the doctor's sovereignty due to the gradual and inevitable increase in this third party's direct influence. And most of all, they were afraid that it was financial institutions that entered this scheme.

The AMA didn't just silently watch the action. For example, they threatened all doctors who participate in payment programs to deprive them of their support. And this was a significant threat, current as membership in the medical society gave the right to compensation for medical malpractice and several other preferences.

Some silver linings appeared in 1938, when the country, shocked by the Great Depression, learned to live under the conditions of the reforms of President Franklin Roosevelt. The new accents of the state policy instilled in people confidence in the correctness of their steps. And the increased attention to health care, against this background, looked quite logical and correct. TIME magazine wrote in 1938: “hard times for doctors and patients, changing public attitudes made doctors think about new ways of providing medical care”.

And then the frightening factor, which we wrote about earlier, came into effect. The apparent threat of a federal initiative to clean up the industry so scared the medical industry regulators that they considered health insurance the lesser evil.

It goes without saying that nothing good will come of it when you are forced to take a step under fear. Insurance companies were imposed on the insurance model as an uncontested option to retain their power and try not to let strangers into medical relationships. It provided for a fee-for-service model. Insurers were reluctant to accept these conditions, believing that these actions would lead to even greater chaos. Such opposition only convinced the medical community that they were right.

The first insurance policies were very sparse and covered almost nothing. They often covered up to 10 specific diseases and nothing else. But that was not the point. The main thing was the creation of a precedent, laying the foundation. And, despite the initially poor and limited system, it continues to evolve to this day.

It is believed that this dubious insurance scheme would be eliminated, and a new, better, and more intuitive health insurance vertical would be created. But, World War II intervened. The fact is that even at the time of heated disputes with insurance companies, the AMA actively used the argument that if opponents did not accept their point of view, then all other options would lead to pure socialism. And, against the backdrop of war, the USSR, depressions, recessions, and communist activists, this maxim suddenly became very relevant.

Moreover, the current system was presented as an example of the fact that capitalism and private industry can effectively and efficiently deal with citizens' health, meeting their financial needs, including.

The ensuing anti-communist hysteria and witch-hunt named after Senator Joseph McCarthy only strengthened the awkward and ill-conceived system's position. And after that, it was too late to change something since the local level of legal regulation had already launched its own mechanism, entangling the country with a complex pattern of a cobweb that no one knew how to break.

The nation got used to what was imposed on them. And this is sad. The United States was in a unique position with many alternatives that emerged in the market's natural self-regulation. With the right approach, one, optimal, or several schemes could be chosen, which would improve over time and turn not the Dutch health care system, but ours, into the best in the world.

Many researchers, including Christy Chapin, are confident that a multidisciplinary group practice model with a fixed fee would be the basis for creating an optimal system.

But, greed, vanity, self-confidence gave us consequences, the most terrible of which was the role and importance that insurance companies have today.

Probably, the title of this section does not correspond to reality. All American health care system problems are critical. And, as we said, the main one is the importance and role of health insurance providers.

Today, of course, from the law's point of view, there are no monopolists or cartels in this industry. But, look at these statistics.

Additional Information:

United States; Forbes

It isn't easy to find companies that are engaged in other areas of insurance here. The market is divided among narrow-profile beneficiaries who control it. There are 930 companies in this medical industry and 850 selling life insurance and annuities companies in the country. At the same time, there are 2,500 thousand providers of insurance related to cars and related liability.

Is it a lot or a little? A complex and manipulative question that is not easy to answer. The answers are straightforward to juggle, substituting the desired point of view. On the other hand, in auto insurance, the top five companies control 52% of the market. You can argue as much as you like, but this is a clear bias.

The situation is similar in the healthcare market. Only the share of the top five is 38%.

Additional Information:

Market share data was generated by using the S&P Global market share tool. The companies share of the market is ValuePenguin ¢ | lendifgtree based on its total health enrollment during the year.

To understand these companies' profitability, let's take a look at the revenue of the top 8 players for 2018.

Additional Information:

Market share data was generated by using the S&P Global market share tool. The companies share of the market is ValuePenguin ¢ | lendifgtree based on its total health enrollment during the year.

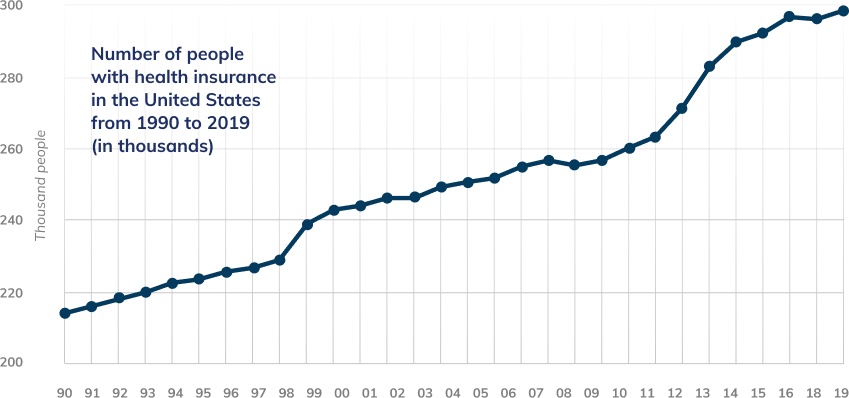

And now, let's turn your attention to the increase in citizens with a medical policy from 1990 to 2019.

And, for a complete picture, let's pay attention to the number of the population without health insurance in 2019 as a percentage for each state.

Additional Information:

United States; Kaiser Family Foundation; US Census Bureau

To look objective, we note that the situation is not so clear-cut upon closer examination of the market leaders in each state. A certain diversification is observed here.

What conclusions can be drawn from everything written? An incredibly socially important industry is divided among a very narrow group of market participants, which acts, literally, the third force in the dialogue between taxpayers and the state on the nation's health. Q, after all, no one will argue that the health and life of a citizen is the highest value for the state?

However, this state of affairs has many interpretations, and we will return to its assessment below. To finalize the American health care system's discussion, let's voice the shortcomings of the rather system that are not so critical.

According to the Commonwealth Fund, Australia, the United Kingdom, and, already mentioned, the Netherlands have the most effective health systems. However, the industry's volume in monetary terms in the United States is much larger than that of all the countries participating in the rating. And, in fact, this is a verdict. If you superimpose the numbers presented above, you can clearly see the scale of the problem and hundreds of its causes. At the same time, we deliberately avoid the system's emotional assessment, not assessing its humanity and fairness.

Although it's worth talking about it, of course, for most countries of the world, health care and medical insurance are not equivalent, but this can be taken as an axiom in the United States. The number of people insured does not always lead to an improvement in health. But, scientists point out that insurance is directly correlated with a decrease in mortality. And, this is a consequence of direct intervention in public health. As of 2017, there were over 27 million uninsured citizens in the United States. One-tenth of them did not have a policy because they did not have the financial ability or documents. Did you know that before President Obama's tenure, that number exceeded 45 million? And this situation is simply incomprehensible for the same UK residents.

Bureaucracy and excessive regulation are other huge problems. A lot of money is spent on administration. In the same Netherlands, everything is much simpler. The standardization of basic benefit packages gives the individual predictable co-payments and understandable conditions while eliminating healthcare providers' administrative burden. That is, insurance coverage is sufficient, but not ideal. This is taken into account immediately and provides flexible changes in implementing the policy, which saves the doctor the time that we spend on long coordination with insurance companies.

Besides, the problems in the United States begin with primary health care. It is disorganized, ineffective, and has limited resources. Lack of funding for primary health care worsens the determination of health and imposes an unnecessarily increased burden on medicine. Criminally little time is devoted to preventive measures to improve public health. And this is the key that will help open the doors to huge money savings.

This is an endless topic of conversation. The insurance industry can be broken down into parts, and all the advantages and disadvantages of each of its components can be specifically and thoroughly analyzed. We may do this shortly. But, for today, we would like to summarize our conversation.

Insurance in the United States is very expensive and costly. Moreover, this applies to any area of your life. Whether you want to protect the risks in the operation of the car, home, finance, or in the healthcare sector, prepare for high costs. The truth is that in other developed countries, all this is much cheaper and the price range on the market is not so high, and the client chooses a company based on its reputation, not price.

But this is not a fundamental problem. The USA is a rich and promising country. And such countries do not promise citizens low prices; they promise the opportunity to earn money. This is on the one hand. On the other hand, such states, among other things, promise justice.

And in relations between citizens, the state as their representative, and insurance institutions, justice is not even close.

A monstrous combination of circumstances, a complex structure of the state machine, and the reverse side of American freedom gave rise to a kind of analog of the golem, which we ourselves have created. Deeper into the topic, you yourself can find out what a narrow circle of companies controls the market share. And the total number of market players in each of the insurance industries does not reflect the picture of fair competition.

American health care system is a kind of quintessence, a collective image of all the system's vices. The system is the most expensive in the world. And, at the same time, it is the most ineffective in comparison with competitive states. We're not going to draw parallels with Russia or Nigeria.

Health insurance is a very bright litmus test that easily demonstrates the industry's negative aspects that can be noticed in other industries only by looking closely.

Why so expensive? This is the first question that arises for everyone who needs to get decent treatment.

Because doctors in the United States prescribe more procedures, they are much more expensive than in other countries. In other countries, the government limits the price of treatment and, in general, is not shy about regulating the industry. No one finds contradictions here, given the incomparable priority of social significance. Medicine receives transparent stimulation and impetus for development in the right direction. For some reason, this does not prevent all patients from receiving advanced and high-quality treatment and market participants - profit.

In the United States, there is no question of profit since everything here revolves around super-profit. Here, the main claim is not even to insurance companies but to American hospitals and pharmaceutical companies, which have great freedom of action to raise prices. At the same time, insurance companies have limited opportunities for negotiations, and, as a result, uninsured patients become the last stage of the food chain.

The terrifying legacy that underlies the existing system grows with new laws and algorithms every year, complicating any attempts to bring it to modern needs. For the past twenty years, every administration seeking to occupy the White House has been talking about the need to change it. Many are taking real action but without much success. However, this is already something because before, anyone who spoke about changes was equated with a communist.

Expansive market growth is also an obvious and worrying problem. The fact is that its position is being strengthened without reference to the general economic situation. We have a confusing relationship between cause and effect. In a normal and healthy economic situation, the insurance industry is growing in parallel with the economy's growth, including investing in it. Now insurers live in their own reality, where national factors affect it. In essence, this situation consists of substituting significant factors, which cannot be the case in a democratic country with a market economy.

Moreover, the socio-political significance of the spheres of life, where insurers are of key importance, is so great that sometimes we are faced with tacit blackmail, which translates into tacit opposition to any change. It is enough to look at the statistics and figures to understand that we have taken a wrong turn somewhere. And there is no need to remind about the taxes that go to the treasury. The issue of filling the budget, in this case, cannot be of paramount importance. Again - because of the critical importance of these relationships for the social sphere.

Nobody pronounces "cartel collusion" out loud, but admit it often comes to mind. State institutions are a clumsy machine, but they are trainable. Otherwise, we simply would not have a chance to survive. The scandals of recent years with privacy at Facebook and Google, with working conditions at Amazon, with loot boxes in video games, give hope to reduce reaction time to modern, completely new challenges. But what about a problem which is almost a hundred years old?

This is a subject of a long and complex discussion. The first thing that comes to mind is centralized regulation, antitrust audit, and a gradual, gradual change in the insurance paradigm itself. In all spheres, but, first of all, in the field of healthcare.

Now, all the industry problems boil down to attempts to adapt to new digital technologies, the struggle among themselves for market coverage. Believe it or not, even global warming, artificial intelligence, and self-driving cars are viewed by insurers as the next critical challenges. They do not get tired of inventing “business models 2.0” and thinking about things that are not global and do not correspond to society's problems. This position only convinces that the current state of affairs fully corresponds to their request.

And this would not be a problem if this state of affairs was consistent with society's request, the clients of these companies.

Remember, we wrote above that the fight against internal socialism and World War II was the key moment that fixed the paradigm of the insurance industry? This usually happens with crises. Fear and loss from them tend to divert our eyes from important transformations. Today's COVID-19 pandemic has every chance, once again, to reinforce those definitions that need to be reformed. This is despiteeven thoughiberately do not ask how much the American health care system is to blame for the catastrophic situation in the United States. However, we kneel before every doctor and medical staff who, sometimes, save the nation at the cost of their lives.

When we get out of this tailspin, where is the guarantee that lobbyists will not seize the opportunity to cement their interests legally?

The situation does not stand. Still, it continues to deteriorate. Putting order and establishing fair rules of the game is a task of national importance, no less. We have always been a country of freedom and human values. If we lose them, we will lose what makes America America and US citizens free people.

Most Recent Articles

We’re secure

Buy with confidence. We offer the highest level of security available on the internet. Powered by Comodo

Call us

| Monday to Friday | 8.00 am-8.00 pm |

| Saturday | 8.30 am-5.00 pm |

| Sunday | 10.00 am-4.00 pm |

For our joint protection, telephone calls may be recorded and/or monitored

1(833) 708-4354why choose us

Car Insurance by States

Health Insurance States

Home Insurance States

Life Insurance States

11440 W. Bernardo Court, San Diego CA 92127

American Insurance - auto, health, home and life insurance provider.

Add new comment